Debt Settlement vs. Debt Consolidation: The Main Difference

The core difference between debt settlement and consolidation comes down to negotiation versus restructuring.

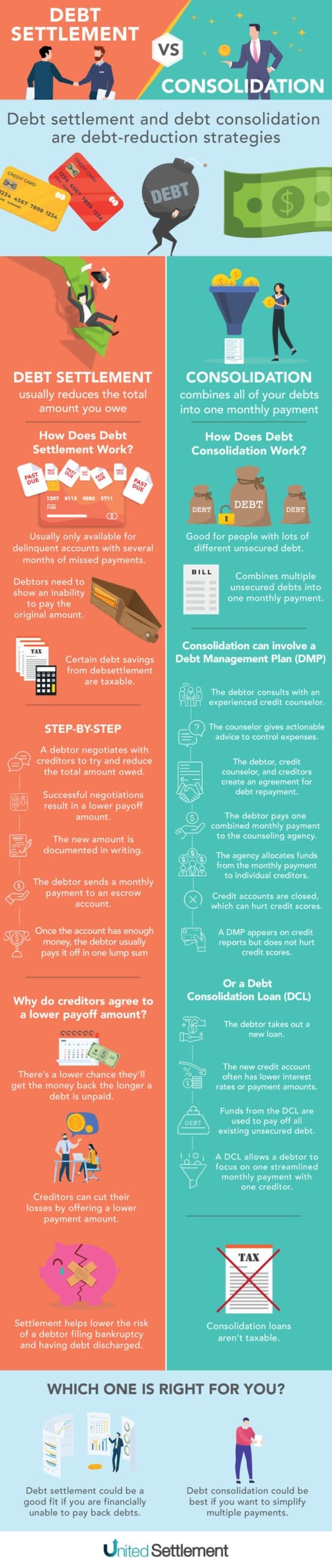

Debt settlement reduces the total amount you owe by negotiating with creditors to accept less than the full balance.

Debt consolidation combines multiple debts into one payment, usually through a loan with new terms.

If you’re weighing credit consolidation vs. debt settlement, the decision often depends on your income stability, credit standing and ability to keep making payments.

Debt Settlement Process

Here’s what you can typically expect from the debt settlement process at a high level:

- Enrolling qualifying unsecured debts

- Setting aside funds in a dedicated account

- Negotiating directly with creditors

- Paying an agreed reduced amount once a settlement is reached

Because settlement focuses on lowering principal balances, it can reduce total repayment amounts in some cases. However, it usually requires stopping or reducing payments during negotiations, which may impact credit scores in the short term.

Debt settlement is typically used by individuals who cannot repay balances in full. When comparing settlement vs. consolidation, the key factor is whether full repayment is financially realistic.

Debt Consolidation Process

Here’s how the debt consolidation process typically works:

- You apply for a consolidation loan or structured payment plan

- Existing debts are paid off

- You make one monthly payment under new terms

This approach does not reduce the amount owed. Instead, it may lower interest rates or extend repayment timelines to make payments more manageable.

For individuals with steady income and fair-to-good credit, consolidation may simplify repayment without negotiation. However, missed payments on the new loan can create additional complications.

Comparing the Processes: Which Is for You?

When comparing debt consolidation vs. debt settlement differences, consider:

- Total balance owed

- Ability to continue making payments

- Credit score impact tolerance

- Long-term cost versus short-term relief

If you can realistically repay your debt with improved terms, consolidation may provide structure without negotiation. If repayment is no longer manageable, settlement may offer a more realistic path forward.

There is no single answer. The appropriate strategy depends on your financial position. A structured financial review allows you to compare both options objectively.

Which Is Better for Credit Card Debt?

For many households, credit cards represent the largest unsecured balances. When evaluating the best option for credit card debt, the math matters.

High interest rates can make minimum payments ineffective at reducing principal. Consolidation may lower interest, but balances remain intact. Settlement, on the other hand, focuses on negotiating lower payoff amounts.

If payments are already behind or becoming unmanageable, settlement may provide relief that consolidation cannot. However, if accounts are current and income is stable, consolidation could preserve credit stability.

Which Option Saves More Money Long-Term?

From a cost perspective, debt settlement often reduces total repayment amounts because creditors agree to accept less than what is owed. Debt consolidation may lower interest, but the full balance must still be repaid.

That said, results vary. Settlement timelines typically range from 24 to 48 months, and savings depend on individual negotiations. Consolidation savings depend on the interest rate secured and repayment discipline.

Choosing between debt settlement and debt consolidation requires reviewing projected payoff amounts side by side. Professional analysis can help estimate comparative costs under each approach.

Who Debt Settlement Is Best For

Debt settlement may be appropriate for individuals who:

- Are significantly behind on payments

- Cannot afford full repayment

- Are facing financial hardship

- Want to reduce principal balances

Debt settlement is commonly chosen by individuals overwhelmed by credit card, medical or personal loan debt who need a structured negotiation approach. If full repayment is not feasible, settlement may be a potential path to resolution.

Who Debt Consolidation Is Best For

Debt consolidation may be a solution for those who:

- Have a steady income

- Maintain fair or good credit

- Can qualify for favorable loan terms

- Want simplified monthly payments

If you’re current on accounts but struggling with multiple due dates or high interest, consolidation may provide organization without reducing balances. Consider your ability to repay your balances and how the simplicity of consolidation could help.

So… Debt Settlement or Debt Consolidation?

There is no single answer to whether debt settlement is better than consolidation. The best choice depends on your goals and your financial reality. If your priority is lowering total debt and repayment feels impossible, settlement may offer a path toward meaningful reduction. If your goal is simplification and you can repay what you owe, consolidation may be the right fit.

Comparing both strategies side by side can help clarify which aligns best with your financial condition.

Not sure which path fits your financial situation? Talk to a debt expert to compare your options side-by-side before committing.

FAQs

Many people comparing debt settlement vs. debt consolidation have similar concerns about credit impact, speed and flexibility. Below are common questions to help clarify differences.

Is debt settlement better than debt consolidation?

It depends on your ability to repay your balances in full. If repayment is realistic, consolidation may be sufficient. If full repayment is no longer feasible, settlement may reduce what you owe.

Does debt consolidation hurt your credit?

Applying for a consolidation loan may cause a temporary credit inquiry impact. Long-term effects depend on payment consistency and overall credit management.

Can you settle debt without stopping payments?

Most settlement negotiations occur after accounts become delinquent, though circumstances vary. Each creditor’s policies differ.

What is the fastest way to get out of debt?

Speed depends on income, total balance and chosen strategy. Aggressive repayment under consolidation can be faster if affordable. Settlement timelines typically depend on negotiation progress and funding availability.